Why our governments are to blame for your rising interest rates

Like most other people, I was unsurprised by the Reserve Bank of Australia (RBA)’s 5th May decision to increase rates for the third consecutive time this year. Nevertheless, this decision to hike rates by 25 basis points to 4.35% does mean we’re back to the 12-year high we thankfully haven’t seen since December 2024.

Then again, inflation is no longer easing as it was from late last year to earlier this year; instead, it’s experiencing a sharp turnaround. The latest Consumer Price Index (CPI) data shows inflation rose to 4.6% in the 12 months to March 2026, up from 3.7% in February. This is a far cry from the RBA’s 2%-to-3% target range.

In its post-announcements press release on 5th May, the RBA pointed to the Middle East war as a key reason for the inflation reversal, as it had “resulted in sharply higher fuel and related commodity prices.”

Watching RBA governor Michele Bullock face the national media, I understood yet again how and why most Aussies point the finger of blame at our central bank after rate-hike announcements, with a firm focus on Ms Bullock.

But I’ve rarely, if ever, been one of these people, and for good reason. Firstly, the RBA is an independent body, separate from our government, although, as its website states, it is accountable to the Australian Parliament for its actions.

So, with this in mind, I’m going to take a stand and aim my frustrations at those I consider the true villains for increasing interest rates. In my opinion, it’s not to Ms Bullock, but rather our federal government – and most significantly, our Prime Minister, Anthony Albanese and Treasurer Dr Jim Chalmers.

I maintain this opinion even in the face of recent surveys which suggest Mr Albanese is pretty popular. A special Roy Morgan SMS Poll in April found 83% of Aussies approve of him, or at least, they like his temporary cut to our fuel excises. Recent Redbridge and Freshwater polls also saw Mr Albanese’s net favourability increase by eight points.

At the same time, Newspoll says Mr Albanese’s approval ratings have decreased from 47% to 40% since mid-November 2025.

Either way, I believe our Prime Minister, and his Labor government, should shoulder the blame for many issues – and I’m not the only one to think this.

Middle East war

The conflict has illustrated how clearly dependent we are on other countries for critical resources, such as oil. One News Corp article I read in March stated that Australia has more than 40 years’ worth of shale oil reserves across six basins.

I agree with the pundits who argue that these oil resources wouldn’t be easy to extract or refine and would require billions of dollars…. but that doesn’t diminish the fact that we do actually have them.

Yet Australia has only two operational oil refineries: one in Geelong (which recently caught on fire, thereby dramatically reducing capacity), outside Melbourne, and the other in Brisbane, following BP’s closure of Australia’s largest refinery in Perth in 2021. And so, we import about 90% of our refined liquid fuel from major refineries in Southeast Asia, including Singapore and China. And, where do these countries import oil from? You guessed it: the Middle East.

So, why, as one article put it, does Australia run on the smell of an oily rag?

According to this Strategist article, a big reason for this is due to the costs involved in utilising our own oil resources; or in other words, the “lengthy and circuitous community engagement and regulatory and environmental approvals that add time, cost and complication to any (oil) project, often to the point of unviability.”

One such environmental approval (i.e. delay) related to the “fracking,” or hydraulic fracturing, needed to extract our 40 years’ worth of shale oil from its solid-rock home.

But, as The Strategist says, there are alternatives to fracking, or even needing to use our aging, current oil bases at all, and that’s biofuels. While biofuels are only “theoretically inexhaustible”, the US, India, and Brazil are hoping to develop policies for biofuel production. Here at home, CSIRO and Boeing have also released a “roadmap” for a sustainable aviation fuel industry that uses biofuels.

Unfortunately, such possibilities still need some political will. And in Australia, it is struggling to find this will seriously. Instead, our Prime Minister is exposing everyday Aussies not only to high petrol prices, but also to further hikes in their interest rates. Then there’s the uptick in the cost of crucial everyday needs, such as groceries.

Yes, this is the knock-on effect of Australia’s near-100 % reliance on Middle East oil, which, in the short term, may be economically wiser, but in serious geopolitical times such as we’re currently experiencing, I can only maintain that it is 100% foolish.

And as Ms Bullock said in the post-cash rate press conference, the war is making Australians poorer, thanks to the shock of oil, energy and commodity prices. Ms Bullock’s words were particularly interesting, as they formed part of a conversation that supports my view on the massive expansion of public spending by our largest-ever number of public servants.

High public spending

The May 5th press conference found Ms Bullock openly stating her concerns about Mr Albanese’s government’s high public spending figures, as well as those of Labor’s state governments.

“When we’re running up against capacity constraints, then (governments) do need to think about whether or not there’s ways they can help the inflation problem by looking for ways to constrain demand,” Ms Bullock commented.

Ms Bullock also wasn’t impressed by Treasurer Dr Jim Chalmers’ proposed plan to give every Australian a no-means-tested $200 to $300 income offset, and by other similar ideas. She said that idea would only “make it harder to dampen (buyer) demand”.

At almost the same time, however, Dr Chalmers announced that, along with the Middle East war, the private, not the public, sector was to blame for the recent inflation hikes.

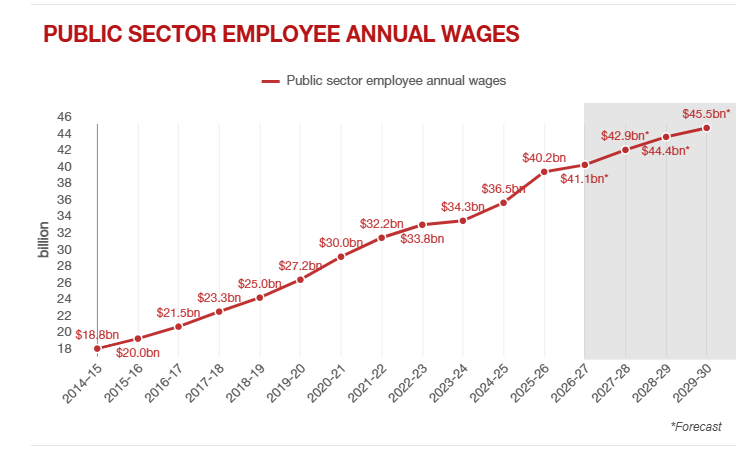

But facts are facts, and not even Dr Chalmers can hide that our public sector has grown by more than double Australia’s population. Or, in other words, in the year ending June 2025, the number of public sector employees grew by about 3.26%, according to the Australian Bureau of Statistics’ (ABS) figures. In comparison, Australia’s overall population growth rose around 1.6%.

As the Institute of Public Affairs (IPA) pointed out, our almost 2.6 million federal, state and local public sector employees now comprise 18% of all employees. Then there’s the fact that these same employees earn an average $20,000 more per annum ($96,309) than private sector workers.

Yet the massive gap between public and private employee numbers is not new. And again, Mr Albanese stands front and centre in my blame game for this, because in the first two years of his Prime Ministerial role, the Australian Public Service (APS) headcount of federal employees surged by 16.4%, or just over 185,000.

And, according to the IPA, we’re set to see more than 107,000 new public employees start work by the end of this June.

The IPA’s Dr Kevin You’s words about these figures are telling: “The only boom sector of the Australian economy is the public service … (yet) the private sector is the engine of economic growth”.

Victoria is even worse!

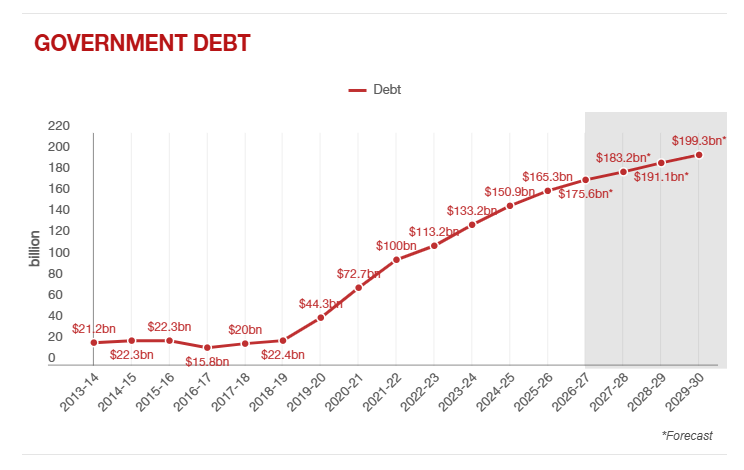

And as we live in Victoria, let’s also single our delusional premier Jacinta Allen, who thinks she can blame the war for Victoria’s reckless spending which is clearly wrong as the public sector wages are skyrocketing at the same time as the “debt bomb” that these financial vandals are leaving Victoria.

The Debt is irrefutable and along with the corruption claims of $15BN+ going to unions, along with a train line (The Suburban Rail Loop) that is completely unfunded and has no business case for it’s construction based on Infrastructure Australia’s findings, that will simply plunge the state of Victoria into more and serious debt.

Tom Elliot, on 3AW’s drive show recently said “we are being run by idiots” and was quick to point out that the single biggest growing expense line in the Victorian State budget is interest and the interest payments piling up from this massive, and sadly, growing debt. He also made a point that in early 2025, the current day state treasurer – Jaclyn Symes – asked everyone in her department to stop referring to “economic” terms when they speak or send her information, as she needs it in plain English… Gee, I wonder why this state is heading down a spiral of debt that is unmanageable!

Immigration increases

These next words will likely not resonate with many of you. But my view is that this issue needs to be discussed, as it is a key reason the cash rate has been hiked three times this year. And again, it’s based on facts.

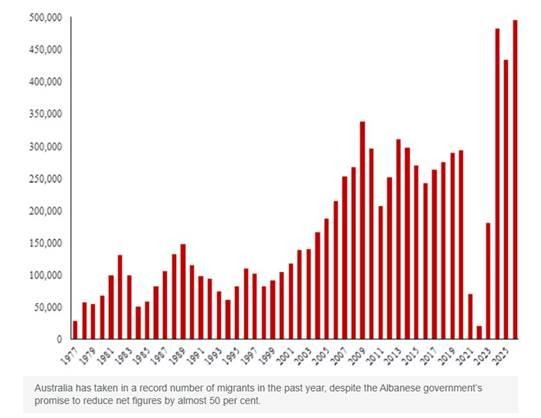

Despite Mr Albanese claiming that his government has reduced immigration by 40%, ABS statistics show that in the year to September 2025, a record number of immigrants came to Australia.

According to an IPA analysis of the ABS’ Overseas Arrivals and Departures report, permanent and long-term arrivals to Australia totalled 415,760 in this period – a figure exceeding the previous record number in 2024 by 6%.

I maintain that immigration numbers have an enormous inflationary impact on our overall economy and, in turn, on our interest rates. After all, each of these migrants needs to secure a place to live, whether to buy or rent, and this is in a country with an overall housing shortage, especially in the rental sector.

And, as the ABS itself comments, regarding its latest CPI statistics, the largest contributor to annual inflation, second only to transport, is housing (+6.5%).

Then we have to consider these migrants’ needs for standard household furnishings and other necessities, such as fridges, washing machines, and beds. Again, the buying of these raises the ante on spending and inflationary impacts.

Talk to a mortgage broker

If you’re one of the many homeowners or potential buyers anxiously watching and waiting for the next RBA announcement, you’re not alone. Nor are you alone in trying to decide whether to drive or walk to work or the shops. But even in this uneasy time, we can help. If you’ve got questions or concerns about your interest rate or your overall mortgage, just reach out to the Intuitive Finance team. In our complimentary strategy sessions, we’ll review your loan and discuss the opportunities available to you and your family.

Andrew Mirams is the Founder and Managing Director of Intuitive Finance, a highly respected and multi-award winning Mortgage Brokerage dealing with clients all over Australia and around the world. Andrew has over 30 year’s experience in the finance industry and has assisted clients to secure over $2 Billion in mortgage lending over his time. Intuitive Finance deals with all aspects of lending from helping first homebuyers, someone wanting to upgrade their home or starting out and experienced investors looking to secure that next investment property, we can assist with all those requirements. We also specialise in working with self-employed clients and getting them the best outcomes, along with Commercial and Asset finance solutions. Intuitive Finance is highly regarded in the industry and has been recognised as a national winner of the MFAA customer service award and also one of the finance industry’s top mortgage employers. Our brokers also feature regularly in the Top 100 mortgage brokers list in Australia.